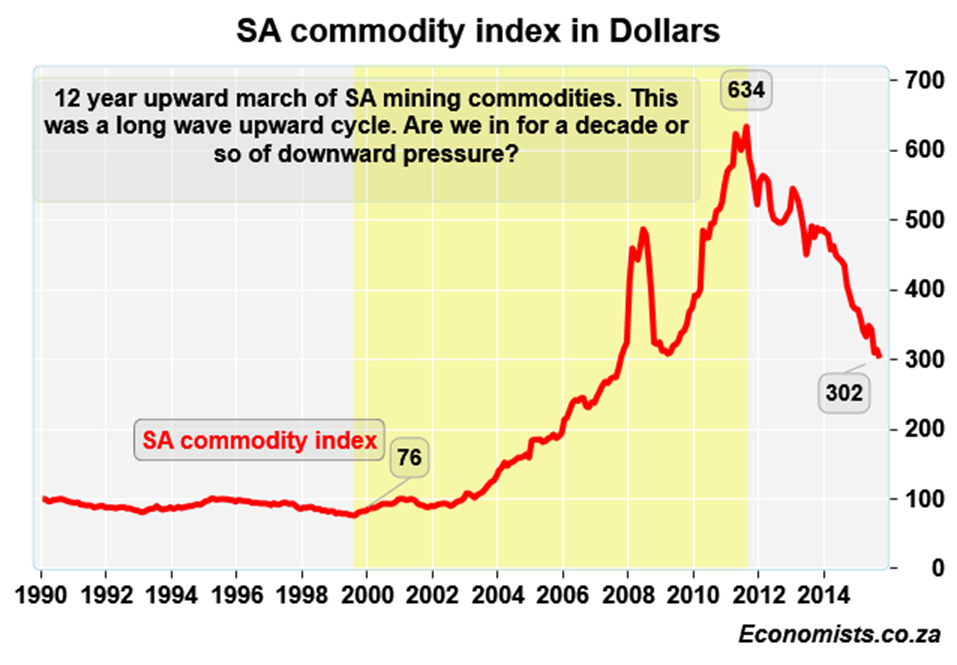

From mid-1999 to 2011 the dollar price of SA commodities increased more than eight-fold and brought with it a relative boom for the South African economy.

Picture: Thinkstock

Since the end of 2011 South African commodity prices have lost more than half their value in dollars. These monthly figures show that South African mining and commodity manufacturing is in serious trouble as the 12-year long rise in commodity prices is over.

The Bank Credit Analyst estimates that we have 40% further to fall on commodities overall and that an ‘overshoot’ is very likely. That indicates that some commodities could still fall by more than say 50-60%. In fact gold fell to about one quarter of its value from the high to the low of the last cycle.

At just over $1 800 per ounce, that may mean that gold will turn at $450 or even less in say 2023. Platinum could in fact go down further as the Volkswagen scandal may cause diesel car sales to decline in huge numbers and platinum could drop to say $400 per ounce or so.

In 2013, according to the annual financial statistics (from Statistics SA), the loss was 3% on assets employed for the whole platinum industry. Since then power costs have increased by 21.7% and labour costs by an estimated 33% or so. The rand price of platinum has declined by about 10% since then.

In rand terms SA commodity prices lost about a quarter of their value since the rand highpoint of January 2014. Moreover the duration of the decline is already longer than the great recession of 2008, although mines and manufacturers have been much more careful about retrenching employees.

The effect of this commodity price decline will be harsh for South Africa.

On the best of days one wants to be positive and there is a positive here and there, but for manufacturing and mining if we do not get a further decline of at least 15% in the rand, the situation will be dire.

By this I mean that the rand will most likely have to decline from R13.80 to about R16.20 to the dollar in the next 18 months – or much of our mines, at present costs, will have to close.

Not fair and not good for inflation as inflation now will be at least 1.5% higher than previous estimates over the next year or two (based on current already-weak rand data). This commodity price collapse will be detrimental to growth and job creation.

Much of my observation is based on the long wave called the Kondratieff cycle or what commentators call the Super Cycle. Many will point out that these sorts of forecasts are extremely subjective and they would be 200% right.

But the infrastructure cycle, or the Kuznets cycle, states that at the beginning of a commodity price collapse much new production still comes on-stream; in coal and iron ore this has been the case for the last few years.

The same holds true for steel and the world now has excess steel production and not just steel capacity, which will take years to sort out as government gives subsidies – making economic decisions all the more political. Platinum is recycled cheaper and never goes away and with the diesel scandal it too is over-producing.

Add the fact that most of our commodities can be stored and are being stored and often recycled and one gets a very negative picture. Excess production is curbing any price gains now and future price gains will be halted by the storage of that extra production before there is any new lift-off in the commodity cycle.

Coal as a major source of power generation may also be over as the world shifts to cleaner (gas and nuclear) and renewable energy. Coal may therefore also not partake in the next upswing, or at least not fully partake in it.

Even oil, which is far more difficult to store, has had a year of 3% over-supply. Oil – our largest import – has added about ten days of extra reserves over the past year as a direct result of this over-supply.

Storage places always run thin when commodity supply outpaces demand for over a while. This has happened and still the world produces too much oil, with extra supply from Iran waiting in the wings.

Lower oil prices bring luck to the country, but certainly the lower SA commodity prices are a curse. We did not use the upcycle as much to our benefit as we should have. We have caught up on new infrastructure just as prices had already started declining in most cases. Rail transport and harbours will struggle to get their money back before the next upswing at least starts to take hold after 2020.

The commodity price declines will bring a new realism to our economic thinking, just when all of that was no longer seen as politically correct. The economic debate has not just drifted further left but ended up being dominated by irresponsible slogans and focuses.

Simply put you cannot strike yourself rich. I think we have seen the last of the long strikes for the next decade or two.

Economic transition

The downturn in the economic cycle for many countries also brings other changes just as it did during the 1980s. South Africa felt the effect of sanctions and lower commodity prices in the mid-80s, which changed the country’s politics completely. The Arab Spring was also brought about by price changes and I suspect more is to follow.

This time the commodity price decline will also lead to some hard head-scratching and I believe we will look at implementing a solution. That solution however may take a few years, as it takes time for the pain to be felt and the analysis to be done.

The early 1980s commodity price decline led to the early 1990s and the political transition of South Africa. The voluntary and relatively peaceful transition was regarded as a miracle, but the realism that all sides faced played a big role.

Now we may be on a similar path but with an economic transition theme. Not the transition that the current politically-correct crowd pushes onto us; but a more realistic picture will form as to what is possible and what is needed.

Simple facts, such as that profits lead to growth and investment which in turn leads to jobs, will come to the fore I optimistically believe.

Brought to you by Moneyweb

Support Local Journalism

Add The Citizen as a Preferred Source on Google and follow us on Google News to see more of our trusted reporting in Google News and Top Stories.