It sounds impossible, but there is actually a way to do it if you start early and make some smart choices.

Picture: iStock

I first covered this topic over four years ago, in an article I did in 2016 that covered how we were planning on investing for our son’s university education.

The cost of tertiary education is something that scares me almost as much as how fast university-related expenses are escalating each year, so I wanted to start putting money away towards this expense as soon as possible. I set up an account pretty much the month he was born.

Well, the months have ticked by and the years flown since then. Our son is almost four, and our initial R500-a-month investment has been doing its thing in the background.

I recently logged into the account to check how things were going.

I was pleasantly surprised!

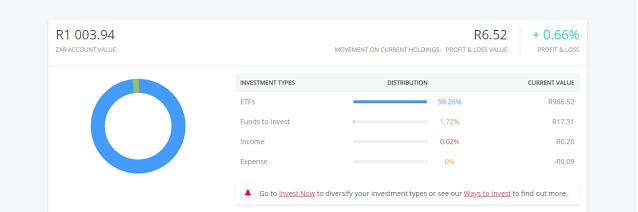

Here’s a screenshot I grabbed.

Source: Stealthy Wealth

Not too shabby – the account has enough to cover more or less one years’ worth of university tuition, and this before my son’s fourth birthday.

A simple linear extrapolation shows there should be enough in this account to cover a four-year course before his 16th birthday (but of course this money is more likely to grow exponentially than linearly, and I am expecting the extra money bunnies that creates to help cover stationery, books and beer too!).

And now I can already hear the questions – is this a tax-free savings account (TFSA)? Where is the account? What did I invest in?

Okay, let’s tackle them one by one.

Should you use a TFSA?

Well, this is a personal choice – but here’s the way I see it.

In short, there were three options available for us to use for our son’s university education investment:

- Invest in a normal account in my son’s name

- Invest in a TFSA in my son’s name

- Invest in an account in my wife’s name

Here is how I evaluated each option.

A normal account in my son’s name

I didn’t like this option – it meant that not only would the account be taxable, but it also meant that my son would have full control of the account on his 18th birthday. As much as I would like to think that I will raise a financially savvy kid, I would hate to see 18 years of disciplined investing get blown on a night in Vegas.

A TFSA in my son’s name

I didn’t like this option either because it also meant the account would be accessible to my son on his 18th birthday. But not only that, making contributions to a TFSA in his name would mean that we would use up some of his lifetime contributions, and even if he did use the money for university, he would not be able to use his full annual lifetime contributions if he wanted to use a TFSA to save for his retirement.

A normal account in my wife’s name

This is the option we went with. By having the account in my wife’s name, we could make sure we use the money for its intended purpose – three to four years of raucous-partying-with-a-sprinkling-of-exams quality education.

Yes, there may be some tax implications doing it this way – but that is why the account is in my wife’s name and not mine.

My wife is in a lower tax bracket than me, so any tax she ends up paying will be much gentler than if it were in my name.

But this is probably a non-issue in any event – I suspect the current capital gains tax (CGT) exemption of R40 000 will be enough to keep us from paying any CGT on the investment.

Where is the account?

We opened the account at EasyEquities – no annual fees, no minimums, super-cheap brokerage and the full range of exchange-traded funds (ETFs) to choose from. In my view it doesn’t get better than that.

If you want to do the same, opening an account at EasyEquities is pretty straightforward (I did a full blow-by-blow in this post).

What are we investing in?

In my view, you can make investing for your child’s education pretty complicated pretty quickly – for example, the education policies you might have seen are made to sound totally legit (I mean, they even have education in the name!). But these are usually just a fancy name for what is likely a complicated and fee-loaded endowment structure with expensive underlying investments that are more likely to send the provider’s/financial advisor’s kids to university than your own.

For me, a long-term investment like this is as easy as choosing the cheapest and most diversified ETF – the Satrix MSCI World (read more on why I like it so much here). Since this investment is for the long term (still around14 years to go) I am happy to just buy that and let it run.

As my son’s university date gets closer I may start selling out (while at the same time harvesting some tax using the annual R40 000 CGT exemption) and move the investment into something more defensive like cash. But I haven’t given too much thought to that for now. That is me-one-decade-from-now’s problem to deal with.

Investing for multiple children

Okay, and what about my other son?

Well I am doing the exact same thing – the Satrix MSCI World ETF in an account in my wife’s name.

Source: Stealthy Wealth

As you can see, he is still in the I-have-just been-born and parents-sleep-is-overrated phase of his life, so we are just getting started with this account.

The reason we opened separate accounts?

I guess having two separate accounts makes it easier for me to account for and track. And since there is no additional cost for having multiple accounts at EasyEquities, why not?

So that’s pretty much our way of planning ahead for possible University expenses in the future. I would love to hear if anyone else is doing something similar, or if you have a different approach? Please share your thoughts in the comments.

(Oh, and by the way – if you want to start planning and investing for your own children, you may find this article and free calculator download helpful.)