The new Minister of Finance becomes the fourth official to lead Treasury in just under two years.

Minister Malusi Gigaba. Picture by Petros Rapule

South African President, Jacob Zuma, has decided to remove the finance minister Pravin Gordhan and his deputy, Mcebisi Jonas, from their posts. Minister Malusi Gigaba, who led the home affairs ministry has been appointed as the new finance minister with Sifiso Buthelezi, a member of parliament, as his deputy. While the two officials are not strangers to public office, they have not served at the National Treasury before.

The new Minister of Finance becomes the fourth official to lead Treasury in just under two years. In that period, South Africa has seen three finance ministers come and go: the respected Nhlanhla Nene got fired and replaced by Des van Rooyen who was, in turn, hastily removed from office to pave way for Pravin Gordhan’s return to Treasury after his earlier tenure. These changes to the economic management cluster of the South African government are the most rapid and unprecedented since the dawn of democracy.

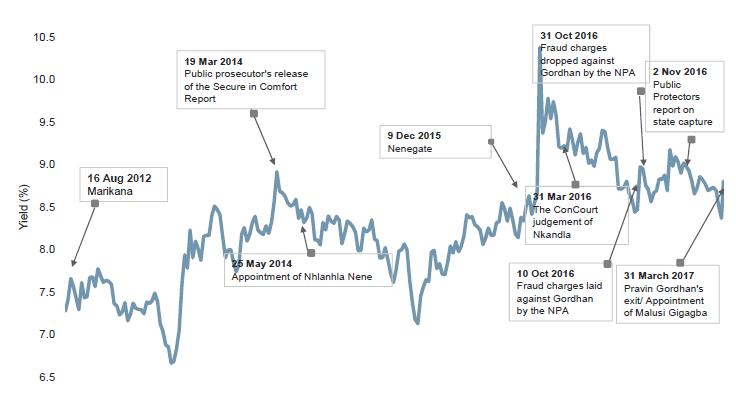

Given such instability at the helm of the National Treasury, financial markets have already responded negatively with the rand selling off sharply. Market participants were aware of the risk that Gordhan would be removed. Even though bond markets became more volatile recently, expressing a heightened sensitivity to developments in the political sphere, we do not see evidence suggesting this risk was fully priced in (see figure 1).

Our view, therefore, is that markets are very likely to react adversely now that the risk has materialised and investors should expect significant volatility in the midst of uncertainty, especially when one considers the factors highlighted below.

Figure 1: Evolution of SA benchmark 10-year government bond yield

Source: Thomson/Reuters Datastream and Investment Solutions

Capital flows

Business confidence has been depressed domestically and foreign investors have begun to sell South African assets. The cumulative outflow in equities in 2016 was around US$9 billion. Although we saw net inflows into South African bonds, on aggregate, there have been portfolio outflows from South Africa. As it is, the Institute of International Finance, a Washington-based global association of financial institutions, has warned that should protectionist policies get implemented in the US by the Trump administration, capital flows (both foreign direct investment and portfolio flows) would face a turbulent time – with countries such as Mexico and South Africa hardest hit.

Need to reaffirm South Africa’s policy position

Investor confidence has been substantially dented by the rapid changes that have taken place at National Treasury. Given such volatility and uncertainty, the new authorities need to communicate that South African institutions remain intact. The independence of the South African Reserve Bank and the judiciary needs to be affirmed. They will also need to demonstrate that fiscal policy will not take a materially different direction from what has been established since 1994. The biggest fear held by investors is whether more populist fiscal policies will be embraced or not.

Credit ratings

Rating agencies have warned repeatedly of the likelihood of downgrading South Africa to non-investment grade should the volatility of the political environment deepen. Although much of the decision will be heavily dependent on what the new Minister of Finance says about fiscal policy and its trajectory, markets are likely to fully price South African debt as junk. After much positive ground gained last year under the leadership of Pravin Gordhan – especially after the relentless effort by business, labour and government, which made such a positive contribution – that work could easily be wiped out should the new authorities exhibit a major deviation from the policy construct put forward at the February 2017/18 National Budget.

Lower returns

Data from Credit Suisse Global Investment Returns Yearbook shows that South Africa has experienced the best after-inflation return in the world of 7.2% for 116 years from 1900-2016. This was better than the 6.8% achieved by Australia, 6.4% by the US, 6.2% by New Zealand and 5.9% by Sweden. Indeed, such a stellar performance is unlikely to be sustained going forward. Given the possible challenges around global capital flows – especially foreign direct investment, which has some positive correlation to equity market returns, combined with the fact that valuations at the Johannesburg Stock Exchange are still above long-term averages – future returns are likely to remain much lower than the lofty gains seen in the last seven years.

Need for diversification

It’s in times like these that investors need to hold on to a diversified and long-term investment strategy. Even as a political storm is once again battering South Africa, history has shown that, in the long-term, markets have the ability to return to fundamentals even when short-term noise, especially from the political sphere, creates much angst.

Lesiba Mothata is chief economist at Investment Solutions.

Brought to you by Moneyweb

For more news your way, follow The Citizen on Facebook and Twitter.

Support Local Journalism

Add The Citizen as a Preferred Source on Google and follow us on Google News to see more of our trusted reporting in Google News and Top Stories.