Slow growth could become the new normal as new regulation bites.

Lewis Furniture store signage in Cape Town. Photo: Gallo Images/Charles Gallo

Shortly after we advised investors to sell Lewis Group in our previous review (FY15), the stock plummeted as it emerged that it mis-sold some of its insurance products. One of the reasons for our call was a regulatory environment growing more stringent for both its insurance and credit sales.

In our previous review we hinted that growth would be difficult to come by and was likely to mimic South Africa’s poor economic growth. In this interim period to end-September, most of Lewis’ growth came from the newly acquired Beares, which was consolidated fully for the first time. Its other two segments, Lewis and Best Home & Electric, experienced lethargic growth synonymous with the challenging economic environment.

The litmus test on household indebtedness is far from convincing, even though recent statistics from credit bureau Transunion show an improvement in credit health. The stagnant economy will make it hard for households to deleverage, which creates a demand-side problem for Lewis, especially in light of the new regulations on credit affordability where the focus is on household savings rather than gross disposable income.

The credit decline rate is likely to soar. The group concedes that adoption of the National Credit Regulator’s affordability assessment regulation has had a negative impact, particularly for the lower LSM segment.

Poor economic fundamentals coupled with the adoption in July of the National Credit Regulator’s affordability assessment regulation have restricted revenue growth. Most of the growth came from the recently acquired Beares, while the affordability assessment regulation ensured that merchandise sales in Lewis and Best Home & Electric didn’t grow. After showing 15.5% growth for the four months to end-July, overall sales growth for the six months to September slowed to 8.8%.

Excluding Beares, merchandise sales in Lewis and Best Home & Electric were flat for the last two months. Beares has a higher cost structure than the group’s other brands and it is expected to take three years to bring its costs down in line with the rest of the group. Excluding Beares, operating expenses rose only 5.4%.

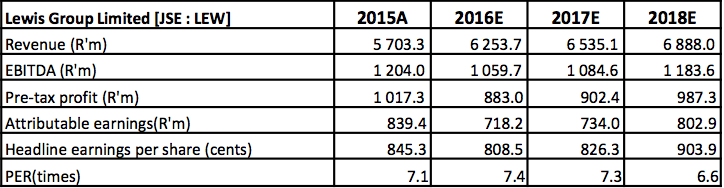

The overall impact was a softening of the operating margin to 14.7% (1H15: 18.4%) and operating profit declined 13.6%. Headline earnings fell 13.4% but the interim dividend was maintained at 215c/share.

Given high levels of indebtedness among the Lewis target market, the adoption of the affordability assessment policy saw the decline rate for credit applications remaining high at 41% (1H15: 41%). Growing bad debts saw debtor costs climb 16.7% and the impairment provision was raised to 24.1% from 22.3%. Debtor costs as a percentage of net debtors rose to 7.4% from 6.8%.

Lewis was accused of selling loss-of-employment insurance to customers who did not qualify. Management says following internal investigations the group identified approximately 15% of cases where such insurance policies were sold to pensioners and self-employed customers. It is refunding the premiums and interest to the tune of R67.1 million.

The regulatory environment presents a real threat to Lewis’ business. While Lewis has started paying back about R67.1 million, the tribunal hearing on that issue is still pending and may come with additional charges. Furthermore, the possibility of credit life insurance capping remains a possibility, including caps on other charges (eg, finance charges) that credit retailers add on their prices.

Three factors are critical to Lewis’ prospects: the economy and household debt; the affordability assessment regulation; and the potential capping of credit life insurance amounts.

Poor economic performance and high household debt coupled with the implementation of the affordability regulation make for pedestrian revenue growth. On the other hand if credit insurance is capped at levels indicated by the credit regulator, it could potentially wipe 11% off Lewis’ top line.

Under normal circumstances we would give Lewis a buy recommendation citing that it was overly pummelled by the market as a result of these insurance charges, as it would have been a one-off cost. Also, management says it will bring down Beares’ cost base so that it is in line with group margins in next three years.

However, with looming changes to the credit regulatory framework, which we have incorporated as a probability in our valuation, we think Lewis is fully valued but with considerable downside risk.

Bull factors

- Acquisition of Beares and possibility of margin expansion in that unit.

- Wide and growing branch network, including small-store format which has lower operating costs.

Bear factors

- Poor economic growth coupled with stringent regulatory developments.

- Negative market sentiment as a result of usury charges may turn off investors.

Nature of business: Lewis Group is an investment holding company which offers a range of furniture and appliances through its network of stores: Lewis, Best Home & Electric, My Home and recently acquired Beares. Monarch Insurance, the group’s financial services subsidiary, provides short- term insurance cover to its more than 690 000 credit customers. The group has more than 700 stores across all major metropolitan areas and a significant presence in rural South Africa, with some of the stores in Botswana, Lesotho, Namibia and Swaziland.

Brought to you by Moneyweb