Markets are long-term machines.

After the weak returns on the JSE over the past five years, it’s difficult to remember where the market was back in 2014. At that point, South African equities had delivered 19.9% per year for the five years following the 2008 financial crisis.

It was an exceptional period of growth, fuelled by the stimulus injected by the world’s central banks. Investors had rarely enjoyed such sustained high returns. However, as Graham Tucker, portfolio manager with the Old Mutual MacroSolutions boutique points out, it was never going to be sustainable.

“What we said at the time was that we were borrowing from the future, because returns were so great,” he says. “The 80-year history told us that this was well above average and that it couldn’t continue.”

At the time, however, there were those who argued that this time was different – that markets could keep going up because there was so much cheap money in the system. There was no end to their optimism.

However, it turned out to be misplaced. Since the highs it reached in mid-2014, the market has stagnated and optimism has turned to despair.

The irony is that once again many investors are saying that this time it is different. Now they believe that the JSE cannot deliver attractive returns ever again because of political uncertainty and local economic weakness.

The historical reality

Where both of these arguments suffer is that they ignore history. A 90-year view of the JSE shows that these periods of outperformance and underperformance are not unprecedented.

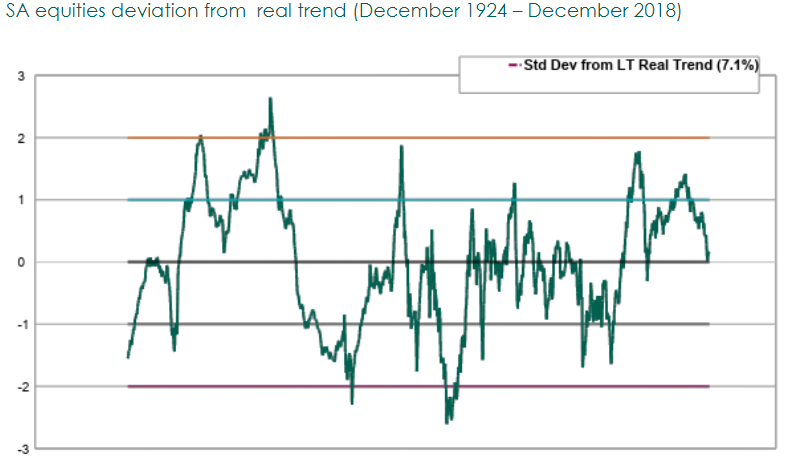

As the graph below shows, the 2014 peak was the sixth time since 1924 that the FTSE/JSE All Share Index moved one standard deviation above its long-term trend in terms of real returns. Those upward market moves are never sustained for long.

Source: Old Mutual Investment Group, MacroSolutions

The lack of growth in the market since then has also only brought the JSE back to its long-term average. We are therefore very far from anything exceptional.

Long-term clarity

The reality is that the market will always go through these cycles, and they will always tend to appear more significant than anything that has happened before while they are taking place. Nothing is as compelling as the present.

However, markets are long-term machines. They have to be seen as such.

An objective assessment of the current state of South Africa would also have to acknowledge that the country has been in far worse economic positions than it finds itself in now. In the 1980s, the country lost billions of dollars as foreign companies withdrew and sanctions put a stop to investment flows. The country’s debt levels had grown to such an extent that it was on the verge of defaulting.

For much of that decade, GDP growth was also zero or negative. By the end of the 1980s South Africa’s per capita GDP had fallen back to the levels it had been at in 1970.

The JSE had not been a great place to be invested either. The 1987 market crash wiped out over 20% of its value in a single day, and this followed negative years in 1981 and 1984. Returns were below trend for most of this decade.

At that point, if recent market performance and the state of the country were anyone’s criteria for investing, the JSE would not have been an unappealing choice. Yet, for the 40 years since, local equities have delivered an annualised return of 17.9%.

What matters is the future

“Too often as investors we are reactive, and often those reactions are exactly the wrong action to take,” says Tucker. “We need to step back, assess the situation and look forward.”

MacroSolutions believes that if one does that, then the local equity market is now offering good opportunities for the first time in nearly a decade. As the following graph shows, the forward price-to-earnings multiple on the market minus Naspers is currently below its long-term average.

Source: Old Mutual Investment Group, MacroSolutions

This doesn’t mean that the market is exceptionally cheap. However, history suggests that future returns from this point should be in line with what they have been in the past.

“The market has moved back to fair value,” Tucker argues. “We are not back at the same valuations or price levels we saw after the global financial crisis, but we are seeing more opportunities.”

As the graph below illustrates, the real market return (after inflation) over the last 10 years is only slightly below average. It is far better than the worst period the JSE has seen. It also shows that, over the long term, the JSE has always delivered positive outcomes for investors.

Source: Old Mutual Investment Group, MacroSolutions

This is why Tucker argues that investors should be prepared to stay invested in the equity markets. As history has shown, this has been the best way to ensure inflation-beating returns over long periods.

“While a lot of investors are looking to run to cash because of the returns they have observed over the last few years, we are looking forward and seeing more opportunities,” says Tucker. “They are not going to deliver in the next three months or six months, but we are positioning for the long term.”

Originally appeared on Moneyweb

For more news your way, download The Citizen’s app for iOS and Android.