Any financial penalty imposed is a non-event.

A week ago the Independent Regulatory Board for Auditors (IRBA) announced that it was instigating an investigation of its own volition into the 2014 audit of the Guptas’ Linkway Trading (Pty) Ltd that was conducted by KPMG. Besides the potential reputation damage that the global accounting firm might suffer, there are punitive options that IRBA can impose on the firm.

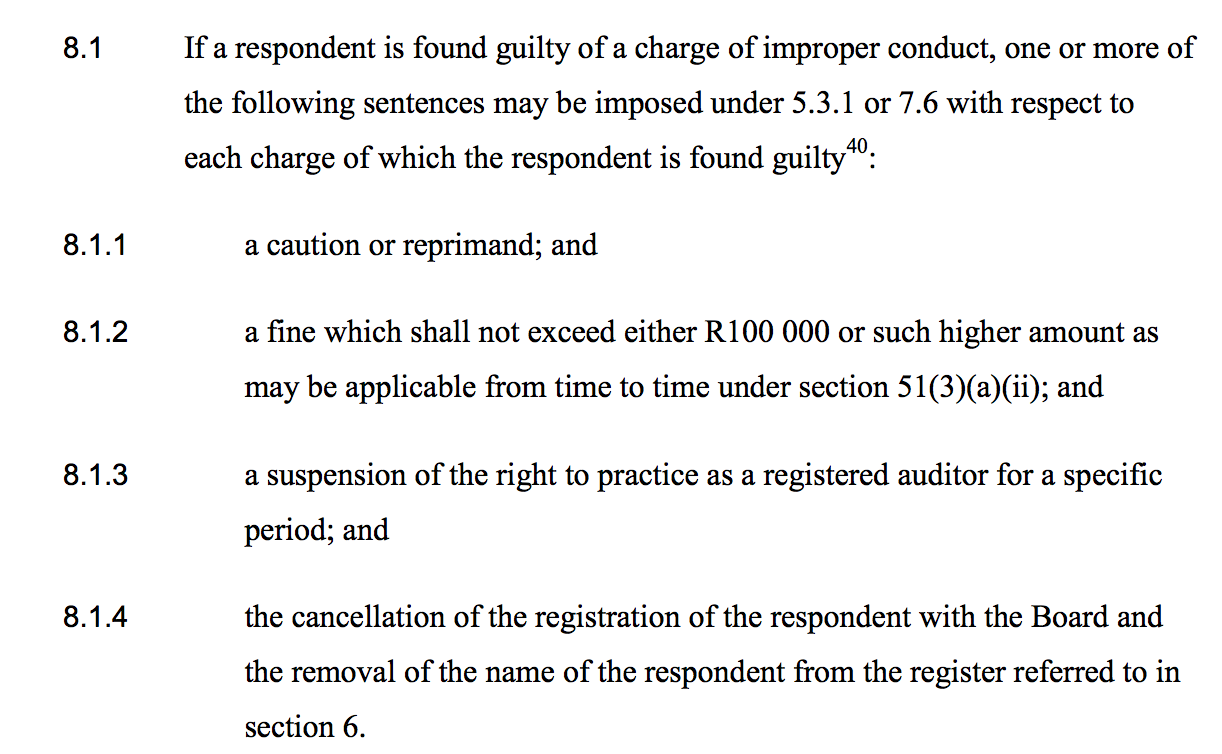

Responsibilities of auditors are encapsulated in the Auditing Profession Act 26 of 2005, and disciplinary rule 8 lays out the sanctions that can be imposed on the auditor responsible, as can be seen from the image below.

Disciplinary sanctions IRBA can impose

Source: IRBA

The fine is hardly likely to cause a partner at KPMG to quiver in their boots, given that they are probably earning close to R650 000 a month with bonuses. But what would hurt an auditor is the right to practice for any amount of time. Moneyweb put follow-up questions to the IRBA and got the following written responses:

MONEYWEB: Further to reading Disciplinary Rule 8, the real threat for KPMG would be “a suspension of the right to practice as a registered auditor for a specific period” – what is the longest suspension IRBA has ever imposed?

IRBA: The most severe sanction would be the cancellation of the registration of the registered auditor concerned and removal of his or her name from the register. The sanction of suspending the right to practice as a registered auditor for a specific period is generally not used.

MONEYWEB: I presume suspension by IRBA would prevent KPMG from practicing as an auditor, would this be a national suspension or limited by geography or cluster?

IRBA: Should the outcome from a Disciplinary Hearing result is removal of a registered auditor from the register, this would be the individuals under investigation and not the audit firm.

MONEYWEB: The next question is on the scope of the investigation; is it within the powers of the IRBA to understand the entire relationship KPMG had with Gupta/Oakbay-related companies to deduce whether this compromised them in any way? (We understand from what is available in the public domain that KPMG had a 15-year relationship with the Guptas, and was its only auditor. Further, the auditor declined to comment on how much “other” work it did for the Guptas – including advisory, consulting and tax – in addition to audit. So will IRBA try and unpack that and understand that?

IRBA: The current investigation is focussed on the allegations pertaining to the 2014 audit of Linkway Trading.

MONEYWEB: Will IRBA’s findings be made public?

IRBA: At the conclusion of the IRBA enforcement processes, the board may, if it deems it appropriate, publish the finding and the sanction imposed.

MONEYWEB: If KPMG disagrees with the findings, what relief in law do they have to challenge it?

IRBA: If KPMG disagrees with the findings of the investigations committee, then it has the right to challenge this and proceed to a disciplinary hearing. The conditions for, and process of disciplinary hearings, are laid out in Section 50 of the Auditing Profession Act.

Rather crucially, should the KPMG partner, Jacques Wessels, be found guilty of neglecting his duties, we will probably never find out the reasons why. Was pressure placed on him to sign off? How conflicted was he? Did the Guptas use their “buying power” to influence his decision? As you can see in the answer to question three, the IRBA’s remit is purely the audit. But what we have learnt from scandals like Worldcom and Enron, is that the objectivity of auditors is called into question when the overall account of the client is substantial to the firm. Otherwise why risk your entire professional reputations and career for peanuts? And therein lies the real danger – if corporate SA believes KPMG has acted unethically in the event of a censure or suspension, KPMG and its partners are going to feel it on the bottom line.

Brought to you by Moneyweb

Support Local Journalism

Add The Citizen as a Preferred Source on Google and follow us on Google News to see more of our trusted reporting in Google News and Top Stories.

![Indian authorities raid Gupta homes show SA making progress - Analyst [VIDEO]](https://media.citizen.co.za/wp-content/uploads/2025/09/Guptas-300x200.jpg)